Automate TradingView By Position

Step 1: Lets' make sure the mode is QUANT

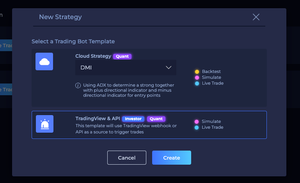

Step 2: Navigate to Strategy and Create a TradingView Strategy

Step 3: Pick USDT Future and your currency

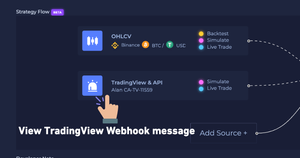

Step 4: Copy Webhook URL & Message to TradingView Alert Box

Step 5: Modify and Save the Alert Message

Note that you replace connectorName and connectorToken

Template Here 👇

{

"connectorName":"REPLACE_NAME",

"connectorToken":"REPLACE_TOKEN",

"log":"{{strategy.order.comment}}",

"entryOrder":{

"value":100,

"mode":"compoundAvailableBalancePercent"

},

"position":{

"side":"{{strategy.market_position}}",

"size":{{strategy.market_position_size}},

"prev_side":"{{strategy.prev_market_position}}",

"prev_size":{{strategy.prev_market_position_size}}

},

"maxWaitPositionReversalSeconds": 20

}

If the orders are too close to each other, use delaySeconds to delay placing orders

{

...

"delaySeconds": 10,

"delaySecondsFilter": "open"

}

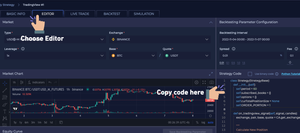

Step 6: Copy the TradingView Python Code template

Copy the code from this GitHub Repository 👇

Details

Expand to see and copy the code

class Strategy(StrategyBase):

def __init__(self):

self.period = 60

self.subscribed_books = {}

self.options = {}

exchange, pair, base, quote = CA.get_exchange_pair()

quote_balance = CA.get_balance(exchange, quote)

self.ca_initial_capital = quote_balance.available

self.ca_total_capital = quote_balance.available

CA.log('Total inital ' + str(quote) + ' quote amount: ' + str(self.ca_total_capital))

def on_tradingview_signal(self, signal, candles):

exchange, pair, base, quote = CA.get_exchange_pair()

leverage = int(CA.get_leverage())

log = signal.get('log')

CA.log('? TradingView log: ' + str(log))

"""

"entryOrder mode": 每次開單的設定

1. "compoundAvailableBalancePercent" 用復利可用資金去下%

2. "noCompoundAvailableBalancePercent" 用單利去下%

3. "totalBalancePercent" 用空倉時的資金固定去下%

4. "fixedTotalBalance" 用固定初始本金去下 需要 size and price

ex.

"entryOrder": {

"value": 100,

"mode": "fixedTotalBalance",

"size": {{strategy.order.contracts}},

"price": {{strategy.order.price}},

}

===

{

"connectorName":"REPLACE_NAME",

"connectorToken":"REPLACE_TOKEN",

"log":"short",

"entryOrder":{

"value":100,

"mode":"compoundAvailableBalancePercent"

},

"position":{

"side":"{{strategy.market_position}}",

"size":{{strategy.market_position_size}},

"prev_side":"{{strategy.prev_market_position}}",

"prev_size":{{strategy.prev_market_position_size}}

}

}

"""

position = signal.get('position')

entryOrder = signal.get('entryOrder')

if not position or not entryOrder:

return CA.log('⛔ Invalid signal, missing position or entryOrder')

tv_order_mode = entryOrder.get("mode") # availableBalancePercent, totalBalancePercent, fixedTotalBalance

tv_order_value = entryOrder.get("value")

tv_order_size = entryOrder.get("size")

tv_order_price = entryOrder.get("price")

tv_position = self.get_position_from_size_and_side(position.get("size"), position.get("side"))

tv_prev_position = self.get_position_from_size_and_side(position.get("prev_size"), position.get("prev_side"))

# 檢查訊號正確性

if tv_order_mode is None or tv_position is None:

return CA.log('⛔ Invalid signal, missing tv_order_mode or tv_position')

ca_position = self.get_ca_position()

quote_balance = CA.get_balance(exchange, quote)

ca_available_capital = quote_balance.available

# 如果不能給之前的倉位那就 預設至 ca_position

if tv_prev_position is None:

tv_prev_position = ca_position

"""

如果反向開單或是加倉

"""

if (abs(tv_position) > abs(tv_prev_position) and tv_position * tv_prev_position >= 0) or tv_position * tv_prev_position < 0:

ca_order_captial = ca_available_capital

# PPC 複利

if tv_order_mode == "compoundAvailableBalancePercent":

ca_order_captial = None

tv_order_percent_of_capitial = tv_order_value

newOrderAmount = dict(percent=tv_order_percent_of_capitial * int(CA.get_leverage())) # default to 1

CA.log("CA開倉比例% " + str(tv_order_percent_of_capitial * int(CA.get_leverage())) + " \n CA下單金額%" + str(tv_order_percent_of_capitial * int(CA.get_leverage())) + " \n CA入場本金$: " + str(self.ca_total_capital) + " \n CA可用資金$: " + str(ca_available_capital))

# 單利

elif tv_order_mode == "noCompoundAvailableBalancePercent":

ca_order_captial = None

diff = ca_available_capital - self.ca_initial_capital

tv_order_percent_of_capitial = tv_order_value

# 賺錢

if diff > 0:

# 算多賺的是幾%

offset_percent = (diff / ca_available_capital) * 100

tv_order_percent_of_capitial = tv_order_value - offset_percent

newOrderAmount = dict(percent=tv_order_percent_of_capitial * int(CA.get_leverage())) # default to 1

CA.log("CA開倉比例% " + str(tv_order_percent_of_capitial * int(CA.get_leverage())) + " \n CA下單金額%" + str(tv_order_percent_of_capitial * int(CA.get_leverage())) + " \n CA入場本金$: " + str(newOrderAmount) + " \n CA可用資金$: " + str(ca_available_capital))

# 下固定金額

elif tv_order_mode == "noCompoundAvailableBalanceNotional":

ca_order_captial = tv_order_value

# 不夠開

if ca_available_capital < tv_order_value:

ca_order_captial = ca_available_capital

notional = ca_order_captial * int(CA.get_leverage()) # default to 1

newOrderAmount = dict(notional = notional)

CA.log( " \n CA下單金額$ " + str(notional) + " \n CA可用資金$: " + str(ca_available_capital))

# 下固定 contract

elif tv_order_mode == "FixedAssetTrade":

newOrderAmount = dict(amount = tv_order_value )

# CA.log( " \n CA下單金額$ " + str(notional) + " \n CA可用資金$: " + str(ca_available_capital))

# PPC 複利 加倉

elif tv_order_mode == "totalBalancePercent":

ca_order_captial = self.ca_total_capital

tv_order_percent_of_capitial = tv_order_value / 100

# 用CA空倉時的金額去下開或加倉的金額

notional = ca_order_captial * tv_order_percent_of_capitial * int(CA.get_leverage()) # default to 1

newOrderAmount = dict(notional = notional)

CA.log("CA開倉比例% " + str(tv_order_percent_of_capitial * 100 * int(CA.get_leverage())) + " \n CA下單金額$ " + str(notional) + " \n CA入場本金$: " + str(self.ca_total_capital) + " \n CA可用資金$: " + str(ca_available_capital))

elif tv_order_mode == "fixedTotalBalance":

ca_order_captial = self.ca_total_capital

# close short -> open long (一個正 一個反) 有一些order數量是反轉時要關艙的 所以要拿掉

if tv_position * tv_prev_position < 0: # 代表倉位方向不一樣

tv_order_size = tv_order_size - abs(tv_prev_position) # 其實就是 tv_position

# 用下單金額和權益去反推TV下單% tv_order_value 是我們的固定本金

tv_order_percent_of_capitial = (tv_order_size * tv_order_price) / tv_order_value

# 用CA空倉時的金額去下開或加倉的金額

notional = ca_order_captial * tv_order_percent_of_capitial * int(CA.get_leverage()) # default to 1

newOrderAmount = dict(notional = notional)

CA.log("CA開倉比例% " + str(tv_order_percent_of_capitial * 100 * int(CA.get_leverage())) + " \n CA下單金額$ " + str(notional) + " \n CA入場本金$: " + str(self.ca_total_capital) + " \n CA可用資金$: " + str(ca_available_capital))

else:

return CA.log("⛔ Invalid tv_order_mode" + str(tv_order_mode))

# close short -> open long 不用管 prev_tv_position 因為我們知道一定會開多 但是要先確保 CA 倉位是對的

if tv_position > 0 and ca_position < 0:

CA.log("先全關空倉在開多")

return CA.place_order(exchange, pair, action='close_short', conditional_order_type='OTO', percent=100,

child_conditional_orders=[{'action': 'open_long', **newOrderAmount}])

# close long -> open short 不用管 prev_tv_position 因為我們知道一定會開空 但是要先確保 CA 倉位是對的

elif tv_position < 0 and ca_position > 0:

CA.log("先全關多倉在開空")

return CA.place_order(exchange, pair, action='close_long', conditional_order_type='OTO', percent=100,

child_conditional_orders=[{'action': 'open_short', **newOrderAmount}])

# CA 倉位是在對的方向

action = "open_long" if tv_position > 0 else "open_short"

CA.log("newOrderAmount" + str(newOrderAmount))

return CA.place_order(exchange, pair, action=action, **newOrderAmount)

# 照比例關艙區

else:

# 沒有倉位不用關

if ca_position == 0:

return CA.log("沒有倉位不用關")

# flat 全關

if tv_position == 0:

action = "close_long" if ca_position > 0 else "close_short"

return CA.place_order(exchange, pair, action=action, percent=100)

elif tv_position > 0 and ca_position < 0:

CA.log("倉位錯亂 全關空倉")

return CA.place_order(exchange, pair, action="close_short", percent=100)

elif tv_position < 0 and ca_position > 0:

CA.log("倉位錯亂 全關多倉")

return CA.place_order(exchange, pair, action="close_long" , percent=100)

# 用TV前和後倉位去看關了多少 不行超過 1

tv_order_percent_of_position = min((tv_prev_position - tv_position) / tv_prev_position, 1) * 100

CA.log("關倉比例% " + str(tv_order_percent_of_position))

action = "close_long" if tv_prev_position > 0 else "close_short"

return CA.place_order(exchange, pair, action=action, percent=tv_order_percent_of_position)

def trade(self, candles):

pass

def on_order_state_change(self, order):

exchange, pair, base, quote = CA.get_exchange_pair()

quote_balance = CA.get_balance(exchange, quote)

ca_available_capital = quote_balance.available

ca_position = self.get_ca_position()

if order.status == CA.OrderStatus.FILLED:

# 看CA的倉位已經用了多少%的本金去開了

ca_position_percent_of_capital = (self.ca_total_capital - ca_available_capital) / self.ca_total_capital

CA.log("? 現在CA倉位數量: " + str(ca_position) + " 本金%: " + str(ca_position_percent_of_capital * 100 * int(CA.get_leverage()))+ " \n CA入場本金$: " + str(self.ca_total_capital) + " \n CA可用資金$: " + str(ca_available_capital))

# 平倉時 設置新的開倉金

if ca_position == 0:

self.ca_total_capital = ca_available_capital

CA.log('新的CA開倉本金: ' + str(self.ca_total_capital))

def get_position_from_size_and_side(self, positionSize, positionSide):

if positionSide is None or positionSize is None:

return None

if positionSide == "long":

return abs(positionSize)

elif positionSide == "short":

return abs(positionSize) * -1

elif positionSide == "flat":

return 0 # not sure

return None

# return current total position: -n 0, +n where n is number of contracts

def get_ca_position(self):

exchange, pair, base, quote = CA.get_exchange_pair()

long_position = CA.get_position(exchange, pair, CA.PositionSide.LONG)

if long_position:

return abs(long_position.total_size)

short_position = CA.get_position(exchange, pair, CA.PositionSide.SHORT)

if short_position:

return -1 * abs(short_position.total_size)

return 0